By Philippa Nantamu and Ian Ortega

A grandmother of one of us had about three cows of the Friesian breed. With these, we had up to 6 or more customers that we supplied daily with milk. The secret was in the productivity of these three cows. The rest of her herd was of local breed. She also had goats, but apart from playfully milking these as kids, the goat milk was largely for the goats. That was many years back in 2004.

20 years later, we have been motivated to revisit this story, but to revisit it from the angle of Uganda’s Dairy Industry, with a specific lens on the processed milk and the milk products. What is the current story of this industry? Where is it coming from? Where is it now? And what can become of it.

The Current Story

Uganda’s raw milk production stands at 3.85 billion litres per annum. Of this, only about 38 percent is processed, 1.46 billion litres. One of the stark ironies of Uganda’s milk story is that Uganda produces more milk than it consumes. Although the Food and Agriculture Organization (FAO) recommends that an adult should consume around 200 to 250 litres of milk a year, in Uganda, an adult only consumes 63 litres of milk.

The Western and Central regions of Uganda make up for most of this annual consumption. This is partly because they are also the biggest producers of milk, but also, because income level is a big driver of milk consumption. The West and Central regions in Uganda have higher per capita incomes than the rest of the regions of the country.

Despite producing more milk than is consumed, Uganda’s dairy industry is also dealing with issues of productivity. The world’s best in class milk productivity per cow is 30 litres per day, however, for the case of Uganda, average milk productivity per cow is 4.96 litres per day. That means, if milk productivity were to rise to this world class average of 30 litres per day, Uganda would be producing up to 23.29 billion litres per annum. Yet, there remains the constraining factor, that Uganda is only processing 38 percent of its raw milk.

Why? It’s both a capacity problem and a consumer problem. A capacity problem in the sense that Uganda doesn’t have the requisite cooling and processing capacities to handle all the milk produced. It’s a consumer problem because for the population that consumes milk, most also make direct purchases of the raw milk, and prefer this to the processed milk. It’s also a perception thing, with most Ugandans preferring the fresh raw milk to the processed milk (that they think has been devalued of its nutrients).

Price wise, raw milk prices at the farm gates range from UGX 800 to UGX 1400 per litre. However, grounded stories from smaller farms say these prices can go as low as UGX 400 per litre. The main producers, also collectors, tend to command the prices of the raw milk. From the farm gate, the milk is then retailed at price ranges of UGX 1671 to UGX 1954.

Once this milk has been processed, the average ex-factories for the processed milk and the milk products is as follows:

- Yoghurt: UGX 4386 per kg

- Whole Milk Powder: UGX 18500 per kg

- UHT Liquid Milk: UGX 2250 per kg

- Pasteurized Milk: UGX 2438 per kg

- Cheese: UGX 23711 per kg

- Butter: UGX 11478 per kg

- Ghee: UGX 13794 per kg

- Casein: UGX 23582 per kg

A big component of Uganda’s processed milk quota is for the export market. The current value of this milk export market is at USD 264.5M. This export market still has potential to grow to a USD 500M capitalization.

The Processed Milk Value Chain

The processed milk value chain is made up of an array of stakeholders. In the direct production cycle, you have the farmers, the milk traders, the transporters, the processors, the consumers, the exporters and the importers.

In the indirect stakeholder groups, you have the government/regulators. This includes mainly the Uganda Dairy Corporation (that’s mandated with the regulation and development of the Dairy Sector) under the Ministry of Agriculture in Uganda. You have the suppliers of packaging products, processing equipment, starter cultures, the distributors, wholesalers and the retailers.

Capacity wise, Uganda has a national milk collection centre cooling capacity of 2.8 million litres, with a total of 193 registered milk tankers for transportation. Uganda has a total installed milk processing capacity of 2.3 million litres of milk per day. Among the big players here includes the Pearl Dairies (producers of Lato Milk), Fresh Dairy/Brookside, Jesa Dairies and Amos Dairies. If Uganda were to process all the milk it currently produces, it would have to raise this capacity to about 10 million litres of milk per day. Even at current milk production, there’s a milk processing capacity problem.

Analysing the Uganda Dairy Industry

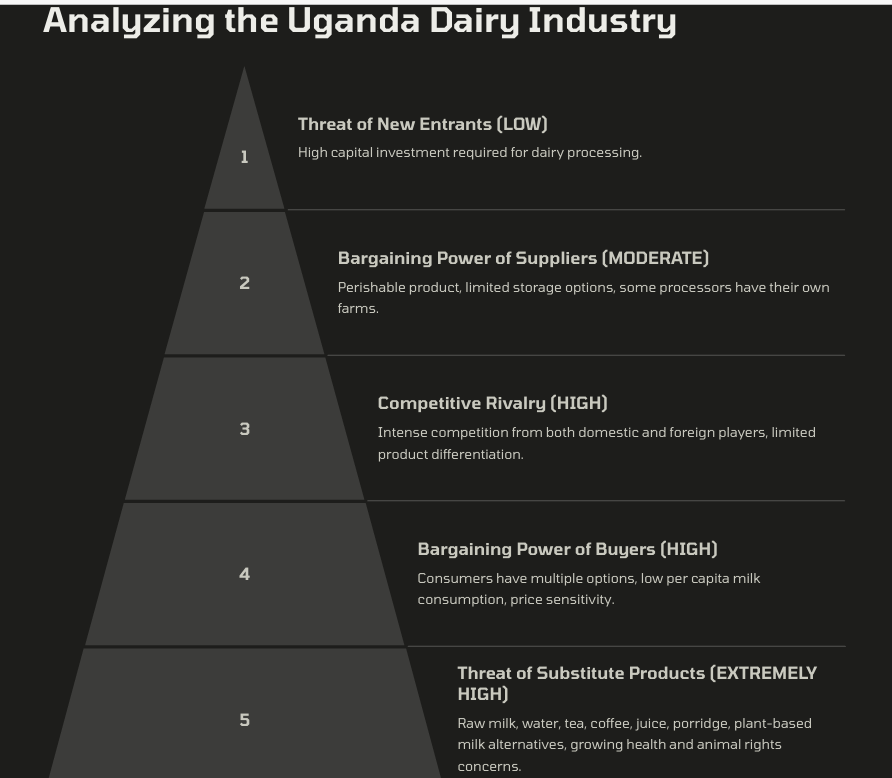

The best framework to understand Uganda’s Dairy Industry is the Porter’s five forces. Through this, we look at the Threat of New Entrants (force one), Bargaining Power of Suppliers (Force Two), Competitive Rivalry (Force Three), Bargaining Power of Buyers (Force Four), and the Threat of substitute products (Force Five).

Force One: Threat of New Entrants (LOW)

Dairy Processing is a capital-intensive venture. To set up a new plant complete with milk chilling tanks, homogenizers, pasteurizers, filling and packaging lines, and boiler systems all together with the buildings and working capital arrangement – one would have to plan with a capital budget range of USD 6.8 million to USD 10.3 million. This makes the threat of new entrants LOW in this industry. Most farmers do not have the bandwidth to forward integrate and establish their own processing plants given the additional activities involved with this extended chain.

Force Two: Bargaining Power of Suppliers (MODERATE)

Milk is a perishable product. Raw milk has a shelf life of about 3 to 5 days (when chilled). Although the DDA has established cooling capacities at the different milk collection centres, the lack of consistency of milking practices affects milk. Thus, the suppliers (farmers) have no option but to fast-track the sale of milk to the traders and the farm buyers. Some milk processors have also established their own dairy farms (this is the case with Jesa Dairies) and thus have low dependence on out-producers. Thus, in our assessment, the bargaining power of suppliers in this industry is MODERATE. Other suppliers to the milk processing industry include; suppliers of cultures and enzymes for the production of cheese, yoghurt ; suppliers of sugar and sweeteners for the flavored milks, suppliers of stabilizers and emulsifiers, flavorings and fortification agents suppliers. There are also suppliers for the Packaging Materials, however most plants will build enough inventory for such. Thus, the suppliers of the raw milk remain the major suppliers, and based on the perishability of their product, the bargaining power is moderated.

Force Three: Competitive Rivalry (HIGH)

Although the internal competition between the milk processors in Uganda may be moderate, the competition is intensified by the foreign players in the market. When Ugandan milk products are placed side by side on the shelves with foreign products, they tend to lose out to the foreign products. Also, given that all players in this industry are largely selling the same kind of product, differentiation is hard in a world where all can guarantee high quality, offer similar flavour options. The competition from raw milk producers/sellers also adds to the competition. Overall, it’s a highly competitive landscape. Players use almost the same distribution chains, they rely on the same family of suppliers, competing for the same consumer. We rate competitive rivalry as HIGH.

Force Four: Bargaining Power of Buyers (HIGH)

The bargaining power of buyers’ aka milk consumers is high. They have other options available to them. And this is evident in the low milk consumption per capita in Uganda. Although WHO recommends about 250 litres of consumption per year, a Ugandan consumes only 63 litres of milk per year. The middle-class that tends to consume most processed milk and milk products is not growing and has also become price sensitive. Industrial buyers such as schools, security forces, prisons and hospitals often will establish their own dairy farms rather than rely on the established players.

Force Five: Threat of Substitute Products (EXTREMELY HIGH)

We already spoke to raw milk as a substitute for processed milk and milk products. However, there’s also other substitutes such as water, tea, coffee, juice, porridge. Growing health concerns have also seen many people revert to plant-based milk options such as almond, oat milk, soy milk and coconut milk. Increasing animal rights concerns are also driving the substitution effect in this industry, the younger Generation Alphas and Generation Zs are raising concerns about how animals are treated during the milking process, the separation from their offspring and issues around animal care at the farm.

Our conclusion is that the Dairy Industry is a highly competitive landscape. However, this presents opportunities for innovation. The Ugandan Population is growing and is also a young population, we see more opportunities to embrace stronger marketing frameworks to drive awareness around the various benefits of milk over the growing plant-based and the need to cater to the population who are unable to consume dairy products. Firms should also think through cost-innovations to competitively drive down the cost of processed milk and increase access to more members at the lower bases of the pyramid. There is immense opportunity for growth in this industry, but it will take a concerted effort of all the players.

How Milk is Processed

The process starts off with milk testing before collection at the farm. In Uganda, this quality assurance happens mainly at the milk collection centres. The milk is then transported in tankers to the Dairy plants. Upon arrival here, milk is tested once again to ensure it’s to the desired quality (such as fat content) and is free from antibiotics.

The process at the Dairy Plant will have storage tankers. From here, milk is separated into cream and skimmed milk by a centrifuge. Alfa Laval is one of the major suppliers of centrifugal separators. Some of the cream will then be remixed back into the skimmed milk, in a process known as standardization, this also enables the milk to have the desired fat content (usually up to 3%). Full Fat is 3%, Semi-skimmed is 2% while skimmed milk is 1% cream.

Once standardization is complete, the homogenization process is started. The aim here is to break up the larger fat droplets and ensure that milk achieves a consistency. When this is complete, it’s then time for heat treatment. Depending on the desired outcome, milk could go through Ultra Heat Treatment at about 135 degrees Celsius, or it could go through extended milk treatment (ESL) at a lesser temperature. Upon heating, milk will then be cooled in a heat exchanger. From here, the milk will be ready for packaging on a filling line and then sent out to the market.

The process largely starts off the same way for the rest of the milk products, with a few differences along the processing lines. The major milk products will thus be:

- UHT milk

- Pasteurized milk

- Powdered Milk

- Cheese

- Butter

- Yoghurt

Who buys milk?

- Households: Purchasing milk for self or family consumption including parents buying milk for their children, individuals for their own needs, or for cooking and baking.

- Businesses:

- Restaurants and Cafes: For preparing coffee, tea, smoothies, desserts, and recipes requiring milk and its byproducts.

- Bakeries and Confectioners: As a key ingredient in baked goods and pastries.

- Food Processing Companies: For creating milk-based products like cheese, yogurt, ice cream, or other processed foods.

- Institutions: Schools, hospitals, and care facilities may buy milk in bulk for meals and nutrition programs.

- Wholesalers and Retailers: Grocery stores or convenience stores purchasing milk from suppliers to sell to consumers.

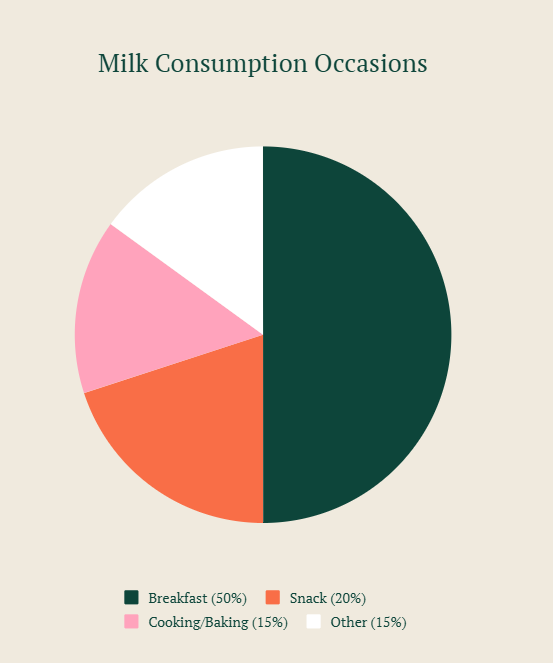

Consumption occasions of milk

1. Daily Routines;

- Breakfast with cereal, porridge, an additive in tea, coffee, base for smoothies or shakes.

- Snack between meals for example paired with cookies, pastries, yoghurt is more consumed as a snack,

- Used in cooking and or baking.

- Often in the evening or night as a soother before bedtime.

2. Health and Wellness

- Dietary Needs, greatly necessary for children’s growth and calcium needs, or used in diets.

- Plant-Based Alternatives for individuals with lactose intolerance or dietary preferences (e.g., almond, soy, coconut, or oat milk).

3. Social and Special Occasions

- Celebrations; in desserts or sweets for events like birthdays or holidays.

- Gatherings where hot beverages like tea or coffee are served such as meetings, family get-togethers, or events.

4. Seasonal Consumption

- Wet and Cold; in Hot chocolate, lattes, and spiced milk drinks.

- Dry and Hot; in Milkshakes, cold coffee, and flavored milk.

5. Convenience Occasions

- On-the-Go: Ready-to-drink flavored milk packs and Grab-and-go coffee.

- In Schools or Offices: Milk cartons for kids during school lunches, coffee milk for office breaks.

What are the consumers’ concerns? ( Key Success Factors in Dairy Industry)

In this burgeoning Dairy industry in Uganda, a few success factors stand out.

- Price

Uganda is a price-sensitive market. Thus, as we explain, being able to lean out the cost structure gives players an advantage to supply milk at the right price points. However, the customer segments will matter. For those playing to the bottom-of-the-pyramid segments, price cannot be ignored.

- Quality

As a product, quality is a competitive set that must feature in the value proposition of any player. It’s with quality that the core differentiation is created in the dairy industry.

The Uganda Dairy Industry Players

Player One: Fresh Dairy/ Brookside Uganda

Formerly owned by Sameer Agricultural Livestock Limited, Fresh Dairy was acquired by Brookside Dairy (a Kenyatta-family firm). Fresh Dairy has a processing capacity of up to 500,000 litres of milk per day. Fresh Dairy aspires to lead the market through quality and performance of its products and customer service.

Fresh Dairy’s product portfolio ranges from the milk category to the yoghurt and cheese categories. In the milk category, it has the flavoured UHT milks, the low-fat UHT milk, and the full cream milk. It plays with the main common flavours of strawberry, vanilla and chocolate. In the butter category, it has both the salted and unsalted butters. It also has a natural ghee product. In the Yoghurt category, it has the plain yoghurt and the flavoured yoghurts (vanilla, mango, mixed berries, and strawberry). It also has an industrial production of full cream milk powder able to supply to institutions such as schools.

Fresh Dairy is highly dependent on the marketing efforts of the holding company – Brookside. In Uganda, its major marketing campaign is limited to sponsorship of the Uganda Secondary School Games. In the past three years, it has not flagged off a major marketing campaign. It also runs a direct-to-consumer delivery line, through a Toll-free phone ordering or whatsapp ordering, a service that was pioneered during the Covid-19 pandemic. Over the years, Fresh Dairy has lost brand equity in terms of share of mind among consumers, with the majority shifting to Jesa and Lato dairy products for their children and households, with those who can afford it occasionally purchasing Brookside flavoured yoghurt. For many Ugandans. For many Ugandans; when was the last time you watched a Fresh Dairy advert or saw a Fresh Dairy billboard? On a side note, the mother company, Brookside has outed some of the best Television Commercials in recent years and has also already added the plant-based milk category with the Almond and Soy milks.

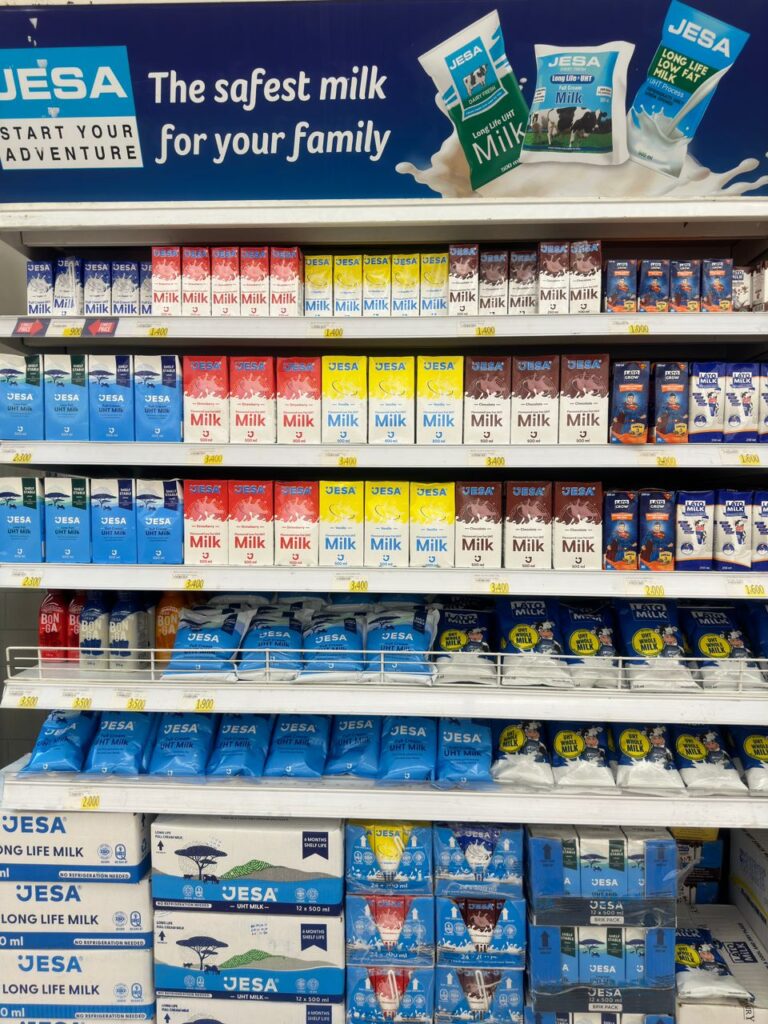

Player Two: Jesa Dairy Limited

Jesa Dairy defines its product categories in threes. First, there is the Yoghurts, then the Milks and finally the Butter and Cream. Jesa’s current installed capacity is 200,000 litres of milk per day. For Ugandans, Jesa has always been associated with quality and taste, thanks to the overall high perceptions of the Mulwana Group and its other products such as the Nice plastics.

In its yoghurt product category, it also has the probiotics, both the lactose free and the probiotic fruit yoghurts. It prides its strategy on its constant innovation. Among the latest innovations is the Jesa Bonga that can be consumed at ambient, without any need for refrigeration. It has also innovated with the juices and has the JESA Jus. For Jesa Dairy, the goal is not to conform the customers to their products, but to conform their products to the customers. It’s to be a customer-centric firm evolving around the behaviour and desires of the consumers.

Jesa came back with a bang in 2010’s and since then has maintained strong availability both physically, it can literally be found everywhere, be it a Kafunda close to home, a petrol forecourt on the way home or at the supermarket where one would go for a planned shopping trip. This has given Jesa a stronghold on the shoppers purse strings and leverage being a Ugandan brand for the Ugandans.

Mentally, Jesa Dairy also runs the best Digital marketing among all the players in Uganda. On its website for example, there’s also a consumer research element to solicit feedback on their Bonga innovation. The Bonga comes in the Coconut, Strawberry and Mango flavours. Also outstanding is the packaging for all its products, something more urban, more futuristic, more aesthetically pleasing than the other players in the market. Jesa sees itself as a lifestyle brand, choosing to term its milk campaigns as ‘Jefreshed, and Jevolutions’. For Jesa, it’s not just about milk, it’s about powering adventures, powering experiences, powering dreams. Jesa also offers fridges to retailers, something that soft drinks and alcoholic beverages companies do. However, Jesa doesn’t have cheese and powdered milk in their product line, yet.

Jesa’s plant is also from a top tier original equipment manufacturer – Filmatic. Many also attribute Jesa Dairy’s transformation to the current CEO, Geoffrey Mulwana, who has embodied his late father’s philosophy of continuous improvement and unending striving towards quality. Jesa’s tagline is aspirational, it speaks beyond features and benefits – Start your Adventure.

Player Three: Pearl Dairy Farm Limited aka Lato Milk

Pearl Dairy boasts of an installed capacity of 500,000 litres per day. To most Ugandans, it’s commonly known as Lato Milk. It’s also the milk that disrupted the East African market. Everybody remembers its disruptive adverts with comedian, Eric Omondi. This was a campaign that was immersed in culture, in our daily lives. It spoke to all age groups. And it built that desire for Lato Milk.

Unlike other players, Lato Milk started off with milk powder production of both whole milk powder and skimmed milk powder, all served in the bulk packaging of 25kg bags. It later ventured into the retail versions of these milk powders with offerings of 900gm, 400gm, tins and 15gm sachets for the mass market (bottom of the pyramid). In 2016, they launched the liquid milk processing line and two years later, they entered the butter category. In the same year, they also ventured into the flavoured milk categories. Like the other players, Lato milk too doesn’t have a cheese category.

Lato also has more product categories than all the other players in the market. This includes juices, instant porridges, infant cereal and butter oil. Their push into

Lato also has more product categories than all the other players in the market. This includes juices, instant porridges, infant cereal and butter oil. With their various sizes and fun “superhero” packaging, they have captivated the children, and parents are finding it easier to prepare porridge every morning for their families because of the instant porridge mix and powdered milk, which are also easily available in many places, similar to Jesa products, when compared to Fresh Dairy.

On its sustainability strategy, Lato Milk has also worked with a polymer company to convert its milk pouches into material for tiles. Part of their aim is towards a zero waste to landfill. One can argue that Lato Milk has positioned itself for the mass market, and all the population at the bottom of the pyramid. They want to be the brand of choice for this market segment, delivering quality at an affordable price.

Player Four: Amos Dairies

For most Ugandans, Amos Dairies may not be a common name in their retail shops. This is largely because Amos Dairies is positioned more as an industrial/commercial producer. Although it has some retail whole milk and full cream milk powder, most of its focus is on industrial scale production.

Among these bulks are 25 kg bags of Instant Whole Milk, Full Cream milk powder and Skimmed milk powder. It also has bulk cow ghee in a 195 kg drum and 15 kg tin. Then it has salted butter in 5 kg, 12 kg and 25 kg packs. Amos Dairies is also heavy on the processing of milk by-products. This includes Whey protein concentrate and Acid casein mesh. For Amos Dairies, the orientation is towards export and thus has less focus on the domestic market. Amos Dairies installed capacity is currently at 600,000 litres of milk per day. Their goal is really to be an integrated manufacturing marketer of quality foods and ingredients.

Opportunity Levers in Uganda’s Dairy Industry

Uganda’s Dairy Industry has the potential to reach an annual market value of USD 500 million. This will be on the backdrop of these interventions outlined by O.G below, you could call them the opportunity levers.

Opportunity Lever One: Marketing

Uganda’s Dairy Industry suffers from a marketing problem. Processed milk and milk products are under-marketed in Uganda. And even when this marketing happens, milk has been purely positioned as a children’s breakfast product. Thus, milk is largely limited to babies, and to the breakfast occasion.

The Dairy Industry players must collaborate on an industry wide marketing campaign to build milk in the minds of Ugandans. The goal is to ensure that Ugandans consume the recommended annual consumption of 250 litres per year. The ideas should be on how to create desire for milk 24/7, to showcase all the occasions during which milk can be consumed, to showcase milk and milk products as a necessary dietary requirement. Why isn’t milk sold in bars? Why is there no milk during lunch time? Why is milk only relegated to breakfast and morning hours? And perhaps in coffee cafes?

Currently, one of the interventions by Uganda Dairy Authority (UDA) is that of the School Milk programme where milk is being rolled out to different schools. The month of June has also been gazetted as the Uganda Dairy month to drive milk awareness. The Dairy Industry must work hard to build a national milk culture. Think of what the AMUL brand became for many Indians.

The AMUL girl is embedded in the minds of every Indian, it’s been part of their life story.

Opportunity Lever Two: Cost Productivity

The cost-structure of milk processing bears heavily on the final retail price whereby the retail price locks out many consumers, especially those at the bottom of the pyramid. How can milk processors drive out costs in their plants? Take an example of the heating and cooling costs. There’s immense opportunity for energy recovery in the milk plants. Solarization is also an opportunity for dairy plants to kill off dependency from the electricity costs. Optimization of boiler efficiencies in the production of steam is a key watch-out. Milk also suffers from wastage costs, that means more vigilance on quality and cleaning in place processes to ensure that there’s zero waste of milk. There’s also potential to innovate around the effluent treatment plants at the Dairy Plants, for example in the production of biogas instead of flaring off these waste treatment gases.

The other lever here is the cost-savings that arise from better efficiencies and effectiveness in the processing plant. From reduced or zero reworks during the process, energy saving initiatives, elements such as robotic milking at the farm (to reduce human intervention) and assure quality of milk.

Opportunity Lever Three: Innovation

There’s opportunity for better feeding, breeding and general care to drive up milk production yields at the farm. Most of this can only come from an agency driven through innovation and experimentation. We cannot run away from the fact that the productive capacity of a Ugandan cow must be improved and scaled.

Digitalization of farm records to ensure better traceability and tracking of output at the farm for every animal. And the ability to integrate farm systems with the plant systems and the market systems. This ensures a single line of supply and demand forecasting.

Opportunity Four: Sustainability/ Animal Rights

The Dairy Industry globally keeps coming under constant criticism around how the animals are treated at the farms, issues around separation of the calves, breaking bonds between mother and calf. The generational shifts in the country, as more Generation Zs, Alphas and now Betas come of age and enter the market implies that these will be issues of concern. There’s now an opportunity for players to demonstrate how they ensure that animal rights are upheld during the production of milk and milk products.

On Sustainability, also demonstration of issues around how waste/effluent from the milk processing is treated. Some milk plants in Uganda still lack certified effluent treatment plants and thus release effluent into the environment. Also, cows are increasingly being highlighted as methane producers through the dung output. The opportunity here is for farmers to shift to higher production breeds, and this will also require the intervention of research from institutions such as NARO to drive better hybrids that are attuned for this environment (disease and weather resistant) while delivering on higher milk production.

Opportunity Lever Five: From Substitution to Complementariness

As more firms and consumers start to shift to plant-based milks. The opportunity to combat this substitution effect is for the Dairy Industry to produce complementariness: that’s to say, combinations such as Almond and Dairy milk, Oats and Dairy Milk, and highlight other contributions such as cappuccino, Frappuccino, to drive the combinations of milk and coffee, milk and tea. The industry should try to address the challenges and drawbacks to all the individuals who are hesitant or unable to consume their dairy products, similar to the way Jesa introduced a “lactose free” yoghurt option to the market. What other products or combinations are growing globally that can also be leveraged for the Ugandan market?

Opportunity Lever Six: End to End Supply Chain Investments

There’s also opportunity for farms to consider a full end to end investment from sourcing to retail. Currently most farms intervene in the middle. By using GPS and route optimization software to improve milk collection logistics, they greatly save on time and fuel. This end-to-end investment will also ensure guarantees on the quality of the processes, and the products. Jesa Dairies for example runs its own farm that it compliments with the cooperatives. However, the opportunity now is to also have milk distributorships and retailer shops. Fresh Dairy back then had opened an opportunity for milk kiosks. It could be time to revisit and reintroduce these. Whereas the marketing will unlock the mental availability, the supply chain optimization unlocks the physical availability. With the analysis of historical sales data, market trends and consumer preferences, predictive demand analysis will assist in controlling overproduction and spoilage.

Opportunity Lever Seven: Data Intelligence

Data intelligence in Ugandan dairy production may greatly increase efficiency, productivity, and profitability, opening up new markets and increasing farmers’ livelihoods while also strengthening the sector.

Use data to detect common farming difficulties, and then provide farmers with personalised training via mobile applications or SMS, as well as training material on feeding, breeding, and health management. Machine learning can assist in predicting milk quality based on variables such as storage conditions, feeding habits, and cow health.

Optimising dairy farming procedures, such as monitoring cattle health and collecting data on milk yield and feeding patterns, would help to prevent illnesses, promote breastfeeding, and increase productivity. Farms can conduct data-driven breast feedings, use weather forecasts to properly manage pasture, water, and paddock usage, and plan for alternative feeding sources as needed.

Farms can use digital platforms to acquire real-time market prices for dairy products, allowing them to negotiate better deals with buyers using dynamic pricing models, deal with seasonal swings, and connect directly with buyers, bypassing intermediaries.

The Future of Milk in Uganda

Having discussed the different opportunity levers in the Dairy industry in Uganda, it’s also important to shine a torch into the future of milk.

One of the things we see is the farm transformation. There’s opportunity for unlocking micro-refrigeration and micro-pasteurization capabilities on most farms. Thus, the next players in the milk industry are going to be microprocessors. This is through forward integration of those that own cows, to go beyond selling of raw milk to becoming micro-processors. For refrigeration companies such as Alfa Laval and GEA, this is also an opportunity to provide access to affordable micro-processing solutions.

We also see the milk retail transformation. First, with more bold retailing channels for milk and milk products. We envisage an ‘Everything Milk’ store. With the everything milk store, it will be a one stop centre for all milk products, brands, and milk needs. From infant formula to yoghurts to plant-based milks. It’s milk taking on centre stage in the retail industry.

Over and above this, is the innovation around more ‘On-the-Go’ milk products. As people become busier, milk products that fulfil daily nutrition needs will come in handy. This could be packaged milkshakes with all the nutrition requirements for the day.

There’s also the coming moment of Milk as a Service (MAAS). This will benchmark the rural milk subscription model but now transferred to the urban world. So instead of consumers going to the shops to look for milk, shops will onboard clients to supply milk at an agreed interval. One will simply have to load their account with more money and the milk shop will deliver as required. This will also help with more demand forecasting as the milk companies will be in the know of their milk consumers universe.